Baby boomers seek clarity on balancing inheritance use with retirement needs and family legacy.

Many baby boomers face important questions about whether and how to use inheritance funds intended for their children during retirement. They often wonder how to balance their own financial comfort with preserving their family’s future wealth. Addressing concerns about budgeting, taxes, and communication with heirs can help retirees make thoughtful decisions that honor both their retirement lifestyle and their financial legacy.

1. How can I ensure my spending won’t affect my children’s financial security later?

Ensure financial security for children by integrating spending into a well-defined plan, keeping in mind both personal and familial priorities. Start by understanding your entire financial picture, distinguishing between personal retirement savings and inheritance. This clarity offers a realistic framework for spending.

Aligning current financial actions with a long-term vision can help maintain stability. Communication with future heirs ensures clarity of intent, fostering financial transparency. An accurate budget reflecting realistic needs allows for judicious spending, balancing day-to-day expenses with legacy aspirations.

2. What are the best ways to budget retirement funds without sacrificing comfort?

Establishing a reliable budget requires a realistic evaluation of anticipated expenses against income streams like pensions and investments. Consider maintaining flexibility for unexpected changes. Aim to cover essential costs while leaving room for leisure, vacationing, and other comforts that enrich life.

Prioritizing needs without excess helps maintain comfort without financial stress. Regularly revisiting and adjusting the budget keeps spending in check, avoiding overextension. Keeping a cushion for leisure, whether a community hobby class or a quiet retreat, maintains joy without jeopardizing overall financial goals.

3. How do I balance enjoying retirement while preserving an inheritance?

Balancing enjoyment during retirement with preserving an inheritance requires a thoughtful approach to spending. Recognizing personal desires and family expectations fosters responsible financial choices. Thoughtfully categorizing expenses aids in differentiating between necessary costs and luxury items.

Mindful expenditure ensures funds last while addressing both current pleasures and enduring legacies. A mix of foresight and flexibility allows celebration of life’s joys without unsettling future financial provisions. Grasping this balance safeguards your welfare and the financial well-being of those you intend to support.

4. Which expenses should I prioritize to maintain independence in later years?

Prioritizing expenses requires weighing independence against luxury. Essential costs such as housing, healthcare, and groceries form the backbone of independent living. They ensure access to comfort and health services crucial for aging gracefully within one’s own domain.

Placing responsibility on non-negotiable needs first supports self-reliance. As these are covered, any surplus funds can enhance lifestyle quality. Activities like art workshops or local theater outings enrich experiences without overshadowing crucial living expenses. This strategy maintains autonomy while allowing bursts of enjoyment.

5. What strategies help stretch retirement savings without depleting assets too soon?

Stretching retirement savings while preventing depletion focuses on prudent financial management. Avoid drawing beyond set limits from savings to mitigate swift fund depletion. Diversifying investment portfolios aids in sustaining income streams across different market conditions, ensuring complemented earnings.

Monthly reviews of spending patterns alert potential adjustments, fostering sustained economic health. Taking a steady approach in spending aligns resources with lifetime needs. Engaging in informed distribution of withdrawals meets essential and discretionary expenditures without compromising overall financial position.

6. How can I plan for unexpected costs without dipping into my inheritance?

Preparation for unexpected costs guards against fund misappropriation. Creating an emergency savings buffer handles unforeseen expenses like medical costs without derailing financial plans. Structuring this safeguard allows continued enjoyment of retirement without unnecessary stress.

Setting aside dedicated savings accounts for emergencies shields principal funds. Unexpected fees, from home repairs to sudden travel needs, find coverage here. This preparation ensures broader funds remain undisturbed, sustaining core financial resilience while aiding smooth navigation of unforeseen life scenarios.

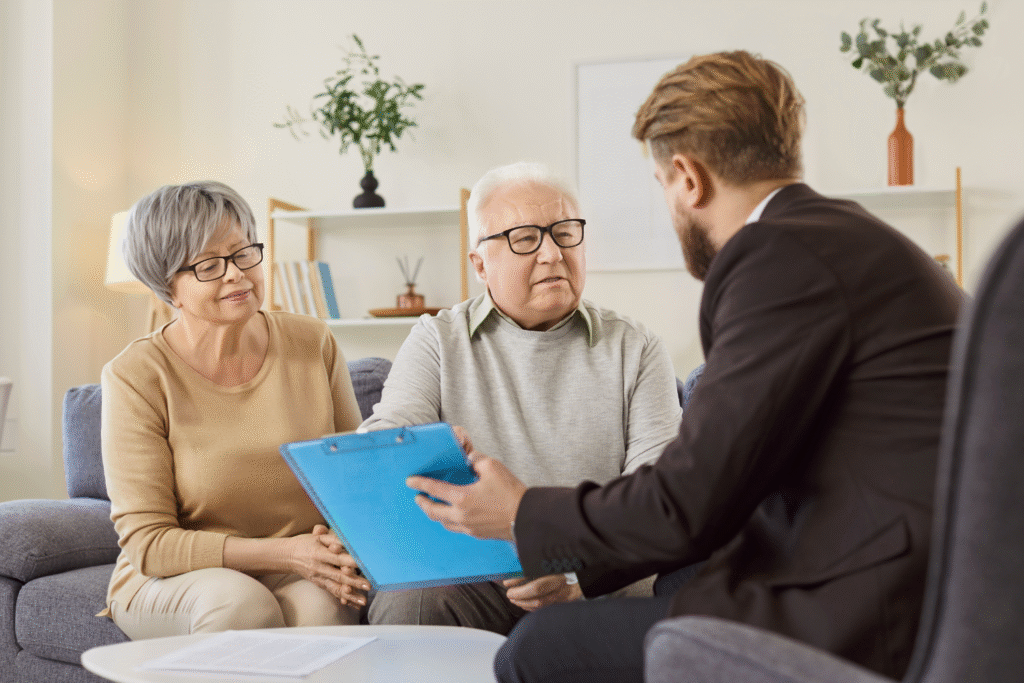

7. Should I involve my children when making major financial decisions in retirement?

Integrating children in major financial decisions can bridge generational understanding. Discussing retirement plans signals transparency, promoting shared responsibility for inheritable assets. This involvement helps clarify individual roles, reducing potential misunderstandings or conflicts.

Such communication fosters mutual respect and aligns expectations, deepening familial relationships. Offering insights into fiscal strategies helps children transition into inheritance with full awareness. Open dialogues create an environment of trust while enhancing future collaborations on financial matters, enriching both retirement and subsequent generational interactions.

8. How do I assess if my current spending is sustainable over my lifetime?

Evaluating current spending against life expectancy estimates evaluates financial sustainability. Regular financial assessments highlight income-expenditure balance and necessary adjustments. Retirement should allow personal indulgences, yet these should remain within a calculated framework, addressing consistent monthly needs while sustaining reserves.

Highlighting areas where spending exceeds sustainability prompts re-evaluation of costs. Social security and other income dictate the feasible pace of expense. Recognizing this fosters longevity of funds, facilitating continued support across more extended periods. Financial health depends on maintaining balanced outflows over time.

9. What steps can I take to protect my assets from inflation impact?

Asset protection against inflation necessitates prudent financial strategy. Diversifying investments into inflation-responsive channels like real estate or stocks guards against devaluation. Periodically adjusting financial portfolios in response to market trends preserves purchasing power over time.

Consistent reviews of assets and economic targets encompass evolving prices. This awareness melds with practiced anticipation of changes, safeguarding core funds. An astute approach that acknowledges market shifts sustains financial project longevity while insulating inherited wealth from economic turbulence.

10. How might my spending choices affect potential estate taxes or fees?

Understanding potential estate taxes and fees elucidates financial implications for the next generation. Carefully navigating tax structures ensures fewer reductions in future inheritance distributions. Enacting long-view financial planning sidelines immediate gains for greater, streamlined estate transition.

Anticipating tax consequences clarifies overall financial footprint left for heirs. Thoughtful preparation can mitigate administrative fees, facilitating smoother asset transitions. Effective strategies echo through generations, fortifying legacies while maximizing inheritable assets for those poised to inherit subsequent financial opportunities.

11. What lifestyle changes can help preserve inheritance without feeling restrictive?

Lifestyle adjustments to conserve inheritance preserve resources without inducing constraints. Optimizing daily expenditures reduces strain on assets, leaving a considerable legacy intact. Activities like community gardening offer fulfilling pastimes that balance enjoyment with fiscal conservation, presenting meaningful engagement without undue financial pressure.

Finding satisfaction in simple pleasures lessens reliance on extravagant spending. Engaging in personally rewarding endeavors draws focus toward life’s fuller experiences. This shift nurtures financial stewardship, maintaining resources throughout retirement while keeping financial health and bequeathal goals aligned.

12. How do I communicate openly with family about my retirement spending plans?

Facilitating open conversations with family about retirement spending demystifies financial intentions. Clarification fosters understanding, ensuring family alignment with legacy visions. Honest dialogues impart financial transparency, reducing speculation about decisions relating to asset deployment.

Such discussions generate inclusive family dynamics, illuminating shared intentions. Protection against misunderstandings encourages more open sharing of perspectives, reinforcing accountability. Continuous communication frames financial integrity, nourishing familial relations while solidifying mutual trust. This approach upholds both private joy and family diplomacy throughout retirement.