These common bills are quietly draining your savings without you even realizing it.

You may not realize it, but there’s a good chance you’re losing money every month to sneaky bills that quietly slip under the radar. After you turn 60, life is supposed to feel a little lighter financially—retirement accounts, pensions, and Social Security should be carrying the load. But instead, many companies count on the fact that you’ll continue to pay for things you no longer need, use, or even remember subscribing to. Over time, these forgotten or unnecessary expenses start to chip away at your hard-earned savings in ways that feel invisible until you take a closer look.

What’s most frustrating is that many of these bills feel harmless on their own—$10 here, $25 there—but added together, they can cost you hundreds or even thousands of dollars every year. The good news is that once you become aware of these common financial drains, you can take simple steps to stop the bleeding and reclaim that money for things that actually improve your life. Let’s shine a light on 13 of the most common bills that could be quietly draining your savings—and how you can finally cut them off for good.

1. Cable TV Costs That Could Be Easily Replaced with Streaming

For years, cable TV felt like a necessary utility—one of those bills you just accepted like water or electricity. But these days, cable packages are often bloated with hundreds of channels you don’t watch, bundled together at prices that continue to climb. Especially for those over 60, it’s easy to fall into the habit of keeping the same plan, even when viewing habits have changed dramatically over time, staff at MTN reported.

Switching to streaming services allows you to pay only for the content you actually enjoy, with far more flexibility and customization. Services like Netflix, Hulu, or Amazon Prime offer robust libraries of movies and shows at a fraction of the cost. Many even provide options for live sports or news if that’s what you value most. By cutting the cable cord and selecting streaming platforms that fit your lifestyle, you could easily save hundreds of dollars every year while still having plenty of entertainment at your fingertips.

2. Landline Bills That Are No Longer Necessary

For decades, the landline was the lifeline of every home—a direct link to family, friends, and emergency services. But with today’s reliable cellular networks, holding on to a traditional landline often serves little purpose other than nostalgia. Yet many seniors continue to pay for this service each month out of habit or a lingering fear of being unreachable, say editors at Mutual of Omaha Mortgage.

The reality is that modern cell phones, combined with Wi-Fi calling, offer crystal-clear connections and flexibility far beyond what a landline provides. Video calls, messaging apps, and even wearable devices have made staying in touch easier than ever before. By finally letting go of the monthly landline bill, you could easily save $20 to $40 every month while embracing modern, more convenient forms of communication that keep you connected to your loved ones wherever you are.

3. Car Insurance Plans That Haven’t Been Updated in Years

Many people set up their car insurance policy years ago and never revisit it, even as their driving habits and vehicle values change significantly over time. As you get older, you may drive less frequently, avoid heavy traffic hours, or switch to an older, fully paid-off vehicle—all factors that can dramatically lower your insurance premiums if you’re proactive about adjusting your plan, according to Rachel Hartman at U.S News.

Insurance companies offer multiple discounts for low mileage, good driving records, and vehicles with advanced safety features. Without periodic reviews, you may be overpaying for coverage that no longer matches your lifestyle. A simple call to your insurance agent to review your policy can often yield substantial savings, sometimes lowering your premiums by several hundred dollars a year without sacrificing the protection you actually need.

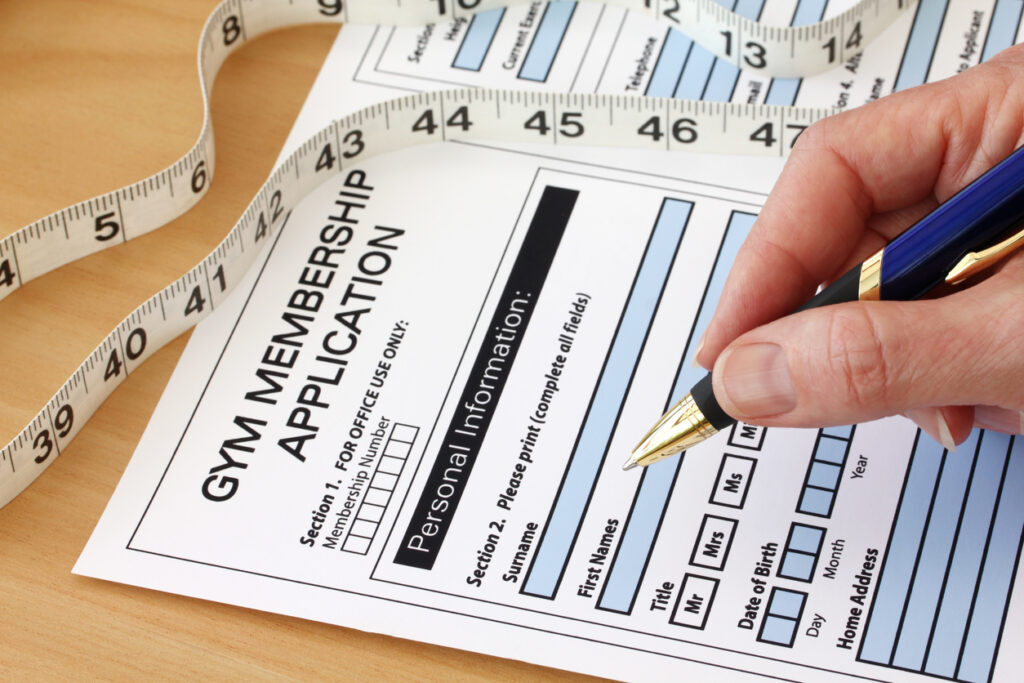

4. Gym Memberships That Are Rarely Used

That gym membership you signed up for with the best of intentions may have quietly transformed into a monthly bill you barely notice but rarely use. Many seniors discover that their workout routines shift as they age—preferring walking, swimming, yoga, or light home exercises over trips to a crowded gym. Yet the membership fee continues to hit your account month after month.

Instead of paying for a facility you seldom visit, explore programs like SilverSneakers, often included with Medicare, or consider low-cost community centers and free online workout programs tailored for your age group. Not only will you save money, but you’ll also find more enjoyable and accessible ways to stay active that better fit your current lifestyle. It’s about choosing fitness that brings you joy rather than draining your wallet.

5. Magazine Subscriptions That Go Unread

In an era where so much content is available online, physical magazine subscriptions can easily become one of those bills that keep renewing long after you’ve stopped reading. Auto-renewal makes it easy to forget about them, and those monthly charges continue to quietly siphon away money for issues that often go straight into a growing stack of unread material.

Taking a few minutes to review your bank and credit card statements can reveal these forgotten subscriptions. If you still enjoy certain magazines, consider switching to digital versions that often cost less and eliminate clutter. Otherwise, canceling these subscriptions altogether frees up space in both your home and your budget while reducing the sense of guilt that comes from seeing those unread piles collect dust.

6. Credit Card Annual Fees That Don’t Offer Value

Many credit cards lure you in with enticing perks—travel rewards, airport lounge access, or high cashback percentages. But as your lifestyle changes, those once-useful benefits may no longer align with how you spend your money. Meanwhile, the card’s hefty annual fee continues to hit your statement year after year.

If you’re not traveling as much or using premium card perks, it may be time to switch to a no-fee or low-fee credit card that better fits your current habits. Many no-annual-fee cards still offer excellent rewards like cashback on groceries or gas, along with strong fraud protection. You’ll retain the convenience of a credit card without wasting hundreds on benefits you no longer use or need.

7. Unused Extended Warranties That No Longer Apply

At the time of purchase, extended warranties seem like a smart safety net to protect big-ticket items. But after a few years, many of those warranties quietly expire or apply to products you’ve long since stopped using or replaced. Meanwhile, some people continue paying for warranty plans that no longer provide meaningful coverage.

Taking a careful inventory of your current extended warranties—and reading the fine print—can reveal which ones are still active and useful. Canceling outdated or unnecessary coverage reclaims wasted dollars and simplifies your financial responsibilities. Plus, many appliances and electronics naturally depreciate to the point where the cost of repairs wouldn’t justify keeping extended coverage anyway.

8. Premium Cable Channels That Never Get Watched

Those add-on premium channels like HBO, Showtime, and Starz may have been exciting when you first subscribed, but how often do you really watch them now? It’s easy to let these extra charges accumulate, especially when bundled into larger cable or streaming packages that hide the true cost month to month.

If your viewing habits have shifted toward Netflix, Hulu, or Amazon Prime, cutting these premium channels can save you $50 or more each month. Many of these networks now offer standalone streaming options you can turn on and off as desired, giving you far more flexibility. Trimming down your subscription stack helps you focus on the content you actually enjoy without feeling nickel-and-dimed by services you rarely use.

9. Overpriced Prescription Medications That Could Be Cheaper

Prescription costs can vary dramatically depending on where you fill them, and many people unknowingly overpay simply because they’ve always used the same pharmacy. Especially for seniors on multiple medications, those small price differences can add up to hundreds of dollars a year.

Tools like GoodRx or pharmacy discount programs can reveal surprising savings, often cutting prescription prices in half—or more. Asking your doctor about generic alternatives can also dramatically lower costs without sacrificing effectiveness. By taking a proactive role in managing your prescriptions, you can free up significant portions of your budget while still receiving the medications you need.

10. Identity Theft Protection Plans That Are Redundant

Identity theft protection has become a booming industry, but many people pay for redundant services they don’t actually need. Some credit cards, banks, and insurance policies now include free identity monitoring as part of their benefits, making standalone protection plans unnecessary for many customers.

Before renewing or signing up for expensive identity protection plans, carefully review the coverage you already receive from your existing financial institutions. Canceling overlapping services can save you $10 to $30 or more each month without exposing yourself to additional risk. You’ll maintain the security you need while cutting away another quiet drain on your bank account.

11. Expensive Cell Phone Data Plans That Go Unused

Many seniors continue paying for unlimited data plans they no longer need, especially if they’re mostly using Wi-Fi at home or spending less time traveling. Cellular companies are more than happy to let you keep overpaying for plans designed for heavy users even if your actual data usage is minimal.

Reviewing your recent data usage and discussing senior-specific plans with your provider can reveal better options at a fraction of the cost. Downgrading to a smaller data plan can shave $20 to $50 off your monthly bill while still offering plenty of connectivity for calls, texts, and occasional mobile browsing.

12. Club Memberships That Are No Longer Relevant

Memberships to golf clubs, alumni groups, professional organizations, or hobby clubs often linger long after you’ve stopped actively participating. The fees seem small on paper, but over time, they quietly add up—especially if you’re paying annual dues for multiple organizations that no longer fit your current interests or lifestyle.

Take stock of which memberships you still actively use and enjoy. Canceling or pausing those that no longer bring value frees up money for new experiences, hobbies, or savings goals. You’ll feel lighter knowing your money is being spent on activities that genuinely enrich your life rather than outdated obligations.

13. Unused Streaming and App Subscriptions That Keep Auto-Renewing

Streaming platforms, music apps, fitness programs, cloud storage, and digital services often renew automatically with little fanfare. It’s easy to sign up for a free trial, forget about it, and then continue paying long after you’ve stopped using the service entirely.

Set aside time every few months to review your recurring charges and evaluate which subscriptions you truly use and enjoy. Canceling just a handful of forgotten services could save you hundreds annually. The key is to be deliberate about where your money is going so that your budget reflects your real priorities rather than a pile of forgotten auto-renewals.