Soaring healthcare costs are delaying key life milestones and reshaping financial plans for many Americans

The rising costs of health insurance in the U.S. are doing more than straining budgets—they’re recalibrating dreams. From monthly premiums to deductibles and out-of-pocket expenses, healthcare spending is now a central factor in whether and how people buy homes, start families, or launch careers. Experts from the Harvard T.H. Chan School of Public Health note that these insurance and drug costs increasingly limit economic mobility and long-term financial stability.

1. Soaring premiums make homeownership feel financially out of reach.

Premiums—the fixed monthly cost of having health insurance—have surged in recent years, especially for those without employer support. For some households, they rival a second rent payment, straining budgets already stretched by housing prices and everyday essentials.

With several hundred dollars going toward premiums before care even begins, entry into the housing market becomes harder. A couple paying steep premiums might delay saving for a down payment, choosing to rent longer while juggling health coverage and other costs that chip away at financial momentum.

2. Medical bills can derail plans to start a small business.

Starting a small business often means stepping away from employer-sponsored insurance, a risky leap in the current system. Without a group plan, self-employed individuals face higher premiums and fewer protections, making solo ventures financially daunting from the outset.

Unpredictable bills add another layer of risk. A single injury can trigger thousands in out-of-pocket costs, forcing entrepreneurs to drain startup funds or push projects further out. The dream of working for oneself sometimes stalls not from lack of skill, but from the cost of getting sick.

3. Monthly costs delay milestones like marriage or growing a family.

Beyond the steep monthly premiums, many plans include deductibles and copays that add up fast. Combined, these expenses can consume funds once earmarked for big life moments like weddings, adoptions, or a larger apartment in a new school district.

When each trip to the doctor punches a hole in the household budget, couples often put off major transitions. That financial squeeze doesn’t always show in spreadsheets, but it’s felt during dinner-table decisions about timing and priorities—a quiet shift in when or whether to expand a family.

4. Choosing jobs based on benefits limits career exploration and growth.

Full-time roles with generous benefits often lure workers to stay put, even if their skills stretch beyond the job. Health coverage can become the tether that keeps someone locked into a position that no longer fits their goals or values.

The trade-off can feel especially rigid in industries without portable or freelance-friendly insurance options. A graphic designer with ambitions to consult might delay the move for years, not for lack of clients but fear of losing coverage they can’t afford to replicate on the private market.

5. High deductibles force people to postpone important medical decisions.

With some deductibles now climbing past four figures, many people face a hard choice when non-emergency health concerns arise. That mole check, knee scan, or mental health follow-up often waits as they weigh cost over comfort.

The hesitation isn’t always dramatic—it can show up as an extra month living with pain or putting off a blood test until after tax season. Delayed decisions can snowball, leading to worsening symptoms, longer recoveries, and sometimes larger bills than if addressed earlier.

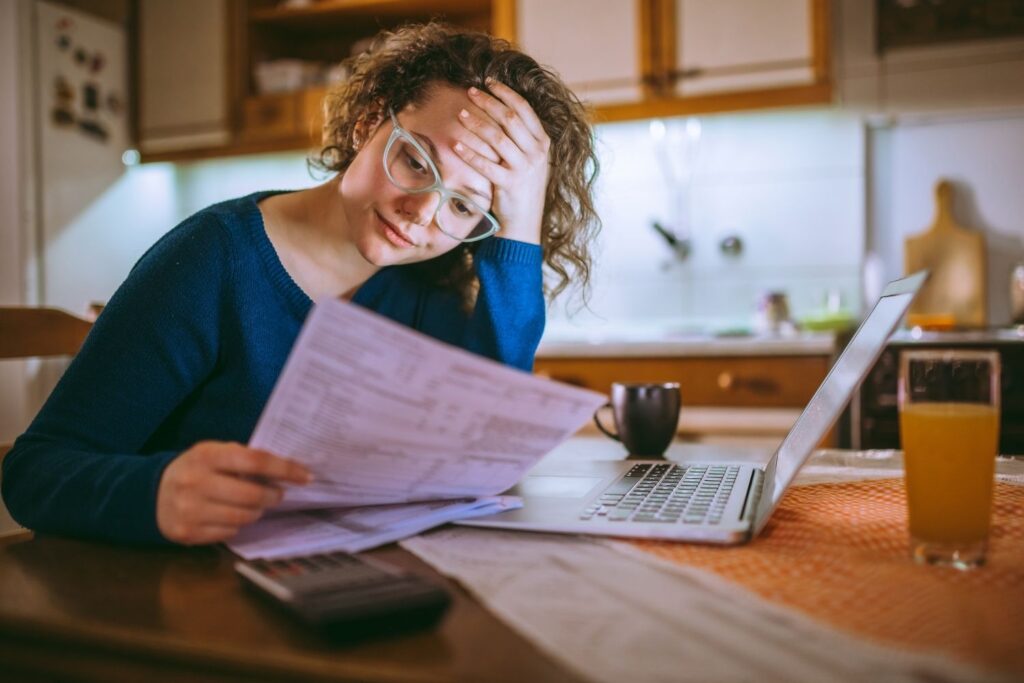

6. Out-of-pocket expenses reduce savings meant for long-term goals.

From retirement accounts to emergency savings, money meant for the future often gets rerouted to pay for prescriptions, labs, and doctor fees not fully covered by insurance. Each new charge subtracts from what could have been long-term security.

Families tapping into savings to cover care may postpone everything from renovations to tuition plans. A health crisis doesn’t just create debt—it interrupts planning. That ripple effect shows up across generations, reshaping expectations around stability and upward mobility.

7. Skipping coverage to save money invites long-term financial stress.

Some skip buying health insurance altogether, hoping to save in the short term. It’s a gamble—one unpaid ambulance ride or emergency room visit can wipe out savings and leave a lasting impact on credit health.

The financial risk often exceeds the perceived savings. Without coverage, even routine care comes at a premium. A dental infection might require up-front cash, leading to delayed treatment and bigger problems. What looks like frugality can become a trap when illness strikes unexpectedly.

8. Retirement planning gets disrupted by unpredictable healthcare costs.

Medicare eligibility is far from a full stop on healthcare spending. Many retirees still face payments through premiums, supplemental plans, and uncovered services, creating a patchwork of costs that don’t always fit within fixed incomes.

Even those with diligent savings can feel whiplash from sudden drug costs or new specialists. One year may require little medical care; the next brings multiple procedures. That unpredictability makes retirement planning more fragile and can pressure older adults to re-enter the workforce or adjust their lifestyle dramatically.

9. Aspirations like travel or education are sidelined by mounting bills.

Ambitions like finishing a degree or visiting extended family overseas often take a back seat to the steady churn of medical payments. For some, every billed service—an MRI, a specialist consult—becomes a detour from personal goals that once felt attainable.

The stress isn’t only financial. When dreams stay paused too long, they can quietly wither under the weight of obligation. A teacher might postpone graduate school after a partner’s surgery eats into tuition savings. The costs live not just on the ledger but in lost time.

10. Fear of losing coverage can discourage risk-taking or career shifts.

People sometimes hold tight to jobs they’ve outgrown for fear of losing coverage in a gap year or transitional role. Health insurance in the U.S. remains largely tied to employment, shaping career moves in ways that don’t always align with ambition.

That fear affects freelancers, creatives, and anyone seeking nontraditional paths. An engineer who’d thrive consulting might avoid the leap, not for lack of clients but because the family’s insurance rides on their corporate ID card. The deterrent works quietly, stalling growth before it starts.

11. Parents may sacrifice kids’ opportunities to cover health expenses.

When parents face steep medical expenses, cuts often happen elsewhere—like arts classes, tutoring, or college tours. Health events trigger hard choices, with children’s enrichment sometimes sacrificed to protect the family’s physical well-being.

A broken arm or unexpected surgery can ripple through soccer dues or school lunch fees in subtle but compounding ways. Even insured families navigating coverage gaps may find themselves pivoting from promotion celebrations to payment plans. That trade-off shapes not just budgets, but childhoods.