Across generations, young adults are reshaping financial goals by favoring comfort over long-term assets

For many young adults today, small luxuries like artisan coffee or skincare routines aren’t just purchases—they’re intentional choices. Faced with a tight housing market, rising costs of living, and evolving lifestyle priorities, homeownership feels increasingly out of reach or even misaligned with personal goals. Instead of saving with no guarantee of payoff, many opt to invest in experiences or comforts that bring daily satisfaction and a sense of control in unpredictable times.

1. Small luxuries offer instant joy that savings accounts can’t match.

A handmade candle, a weekly latte, or a facial once a month—these aren’t extravagances so much as tiny luxuries that provide immediate satisfaction. Unlike slow-growing savings goals, these purchases deliver emotional return on investment right away, offering comfort after long workdays or stress-filled commutes.

Emotional payout matters more when financial goals feel abstract or delayed. A savings account grows quietly, often unnoticed, but the glow of a cafe lamp or the warmth of a cashmere scarf makes the moment better. In tight budgets, it’s easier to value certain joy now over uncertain security later.

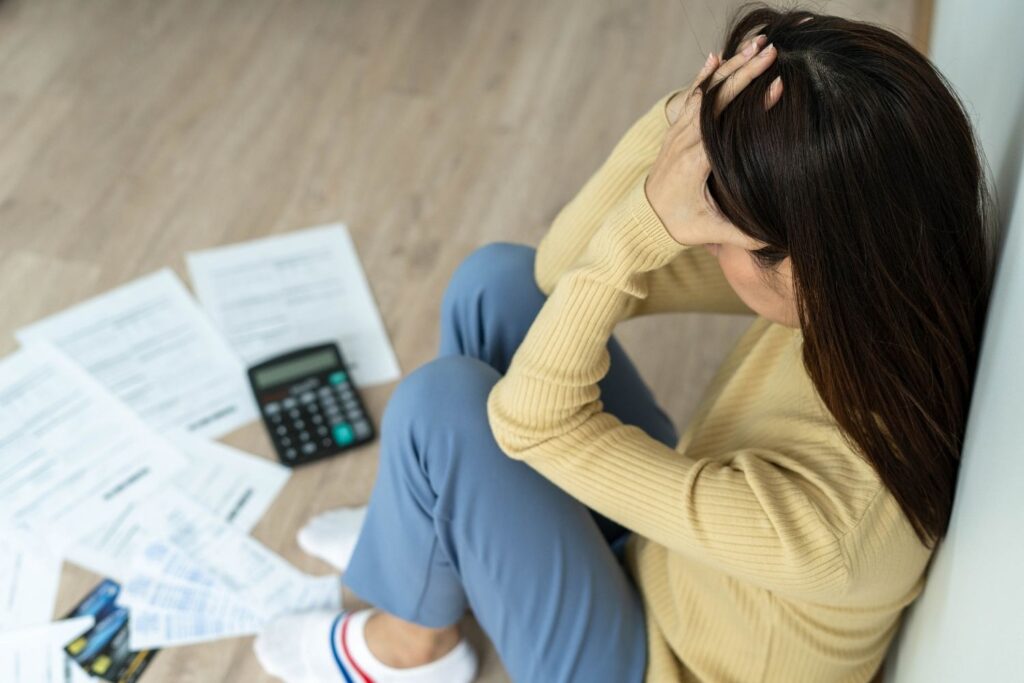

2. Many feel home ownership is out of reach regardless of effort.

Escalating real estate prices and stagnant wages have created a widening gap between effort and outcome in home buying. Many young people, especially in cities, say they could scrimp endlessly and still never afford a down payment on even a starter home.

That mismatch drains motivation. Saving for a house starts to feel like chasing a mirage, especially when student debt and rent already stretch income. By contrast, choosing small delights feels like an act of autonomy—claiming control in a market that often feels rigged against entry-level buyers.

3. Experiences and self-care rank higher than long-term financial goals.

For many younger adults, actions like booking a weekend trip or investing in skincare reflect a shift in what counts as a life well-lived. Joy tied to meaningful moments or daily comfort now rivals the allure of property acquisition decades into the future.

Those priorities don’t signal recklessness. Rather, they reflect an evolving framework of personal value where a solo museum visit or a Sunday massage might provide more emotional return than square footage. When financial stress runs high, emotional resilience becomes its own form of wealth.

4. Flexible lifestyles make long-term housing commitments less appealing.

Month-to-month work schedules, remote jobs, and co-housing arrangements have redefined how younger people think about permanence. A 30-year mortgage in one city can feel like a constraint, not a milestone, for those raised in an era of relocation and reinvention.

Flexible living can support evolving careers and relationships—but it complicates anchoring money in one fixed asset. When life may shift in six months, even an apartment lease might feel too heavy. In that light, many choose convenience, experience, and adaptability over immobile investment.

5. Rapid lifestyle shifts encourage savoring the present over planning ahead.

The pace of change in employment, housing prices, and personal routines makes long-term planning feel futile for some. If cities, jobs, and rent all fluctuate in a year, small stable comforts can feel more rewarding than abstract goals tied to a distant future.

Buying plants for a temporary space or splurging on a local bakery rarely comes from frivolity. It’s often a grounded response to volatility. For many who grew up watching bubbles burst and costs rise, the present holds more promise than the unpredictable horizon ever could.

6. Social media reinforces valuing aesthetic pleasure and daily indulgence.

Photos of frothy coffee, curated bookshelves, and artful breakfasts fill screens daily. These images shape how people judge their own lives, often subtly equating daily aesthetics with personal success or self-worth. Small indulgences become a way to match those visual benchmarks.

Spending choices often carry social weight, even subconsciously. A luxurious-smelling candle might last a month, while a savings deposit offers no immediate sensory reward. Trend-driven platforms emphasize lifestyle optics over financial abstraction, reinforcing short-term spending cues across peer groups and timelines alike.

7. Past financial crises have eroded trust in traditional investments.

Economic setbacks during formative years color how younger generations view financial institutions. Watching retirement funds dissolve or home equity vanish shaped deep skepticism around traditional wealth-building paths—especially ones tied to real estate.

That legacy lingers. Many came of age believing that storing value in big assets doesn’t always work out. Some redirect focus to experiences or consumables that can’t be wiped out by a market downturn. Small luxuries feel safer in part because they’re already paid for—and already enjoyed.

8. Monthly rents leave little room for significant savings toward homes.

After rent, groceries, and monthly bills, little remains for many to put aside. Even with careful planning, the amount left over often won’t close the growing distance to a down payment, especially in high-demand housing markets.

That math changes behavior. When savings can’t make a dent in housing goals, modest spending that boosts happiness starts to feel like a reasonable tradeoff. Buying a record player or dinner out may not move the needle financially, but it changes the day’s tone in ways that matter.

9. Memories and comfort are prioritized over minimalist future planning.

Many choose cozy pleasures—a plush blanket, a comforting dinner, a scent that reminds them of home—not because they reject the future, but because those touches create meaning in unpredictable times. Emotional investments take precedence when stability feels fragile.

Future planning isn’t abandoned, just reprioritized. Keeping a journal, hosting friends, or crafting something by hand builds a kind of wealth not tracked in an app. Soft edges and flavorful meals can buffer against a world that often asks for sacrifice without guarantees.

10. Small treats offer tangible rewards compared to abstract financial goals.

Aromatic body oils or quality tea offer something saving accounts don’t: tangible benefits now. When the future feels uncertain, a good night’s sleep or a warm kitchen moment can matter more than spreadsheets or compound interest charts.

Even tiny luxuries can hold symbolic weight. They represent self-care, dignity, or the satisfaction of choosing what feels right in a moment. While traditional finance goals rely on discipline, these daily treats reward consistency with comfort, making them powerful—even rational—alternatives in many modern budgets.

11. Cultural shifts favor personal well-being over chasing property ownership.

Wider cultural narratives now frame success less around ownership and more around how one feels. Mental health and balanced living edge ahead of status symbols, with property often seen as just one piece—not the pinnacle—of adult life.

Trends in media and conversation reflect this shift. Podcasts celebrate rest, shows spotlight travel and taste, and online communities trade real estate ambition for emotional literacy. Homeownership remains part of the story for some—but far fewer see it as the only ending worth pursuing.