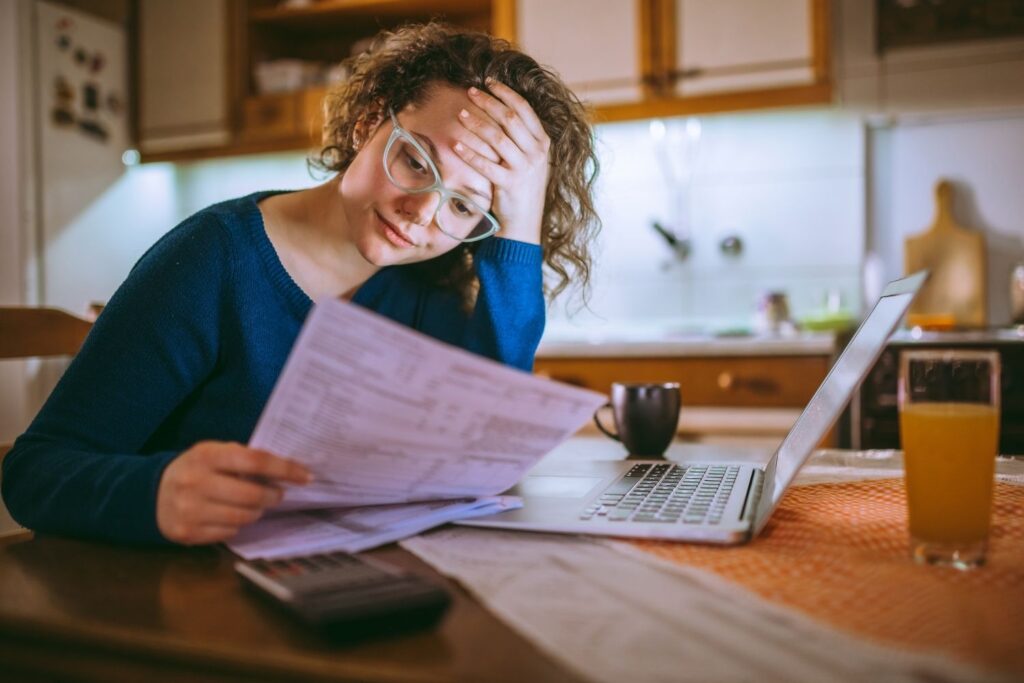

Even in high-income areas, rising debt and shifting economics are straining household financial stability

Credit card delinquencies are breaking the mold by showing up in some of the nation’s wealthiest zip codes. While high earnings often suggest financial security, factors like lifestyle inflation, job volatility, and rising interest rates are reshaping the debt equation for more affluent households. Experts from the Federal Reserve and Brookings Institution note that unsecured debt and high credit utilization are increasingly taking a toll, challenging old assumptions about who feels the strain of financial stress.

1. Rising interest rates are making debt harder to manage.

When interest rates rise, the cost of carrying a balance grows fast. Credit card debt, which is unsecured, becomes more expensive by the month as annual percentage rates float higher. Even minimum payments stretch tighter, especially when people carry multiple cards.

In high-income households, cardholders often assume they’ll pay it off soon. But with interest rates pushing 20 percent or more, monthly charges mount quickly. A five-figure balance on a rewards card can quietly grow heavier than expected, even in homes with polished countertops and two-car garages.

2. Lifestyle inflation in affluent areas can strain monthly budgets.

As incomes increase, spending often follows. Upgrades start small—a new espresso machine, a seasonal ski pass—but over time, they add up. This pattern, known as lifestyle inflation, turns discretionary purchases into fixed expectations.

What feels like routine comfort to one family can silently shift a budget’s balance. Particularly in affluent neighborhoods where social norms tilt upscale, the gap between income and expenses can narrow in subtle ways that debt begins to fill. High earnings don’t always leave room for cushion.

3. Easy access to high credit limits leads to overspending.

Banks tend to offer higher credit limits to borrowers with strong incomes, good credit, or both. In affluent zip codes, consumers may carry several cards with five- or six-figure limits, opening the door to large discretionary purchases on a whim.

But higher limits can dull spending awareness. A $10,000 sofa or premium airline upgrade may not prompt pause when the credit line stretches far beyond that. Over time, those choices stack up against future income, creating rolling balances that become harder to pay off in full.

4. Economic uncertainty is shaking confidence across income levels.

Economic slowdowns tighten uncertainty across the board—not just for lower-income workers. Shifts in financial markets, pending layoffs, or reductions in business earnings stir anxiety, leading some households to rely more on revolving credit.

Among high earners, even a temporary dip in cash flow can expose overcommitments masked by steady paychecks. When optimism dips and costs stay high, debt balances that once seemed manageable can quickly feel less stable—especially if repayment relies partly on future bonuses or investment returns.

5. Job volatility among high earners affects financial stability.

High earners aren’t immune to job loss or pay fluctuations. Commission-based roles, bonuses, or revenue-sharing structures can create wide income swings, even for professionals well into their careers. Sudden changes upend plans fast.

A lapse between roles—or even a six-month bonus delay—can crack open a financial gap. If household spending is structured around past earnings, those who once earned $300,000 may feel pressure long before official hardship hits. Credit balances often rise quietly during these transitions, especially where fixed expenses remain high.

6. Increased borrowing for luxury goods adds long-term debt pressure.

Large purchases like custom furniture, jewelry, or international travel often land on credit first. In wealthier areas, the drive to personalize or optimize luxury often means spending significant amounts upfront, with plans to repay over time.

Over months, these decisions accumulate. Unlike a mortgage or car loan, revolving credit lacks a clear end date, so balances may linger. Even if no one misses a payment, interest builds. Add a layer of volatility, and luxury debt begins transforming into long-term financial drag—even with high monthly deposits.

7. Unexpected medical costs can upset even well-planned finances.

Even with good insurance, a medical event can trigger uncovered expenses. Out-of-network specialists, experimental treatments, or higher deductibles can leave families facing unplanned bills in the tens of thousands.

People in affluent zip codes may assume resources will cover emergencies, but liquid cash doesn’t always keep pace with lifestyle. A single hospital stay with an ICU charge or complex follow-up care may compel short-term borrowing. The result can be debt that lingers far longer than the health issue itself.

8. Real estate costs in wealthy zip codes often outpace incomes.

Housing costs in top-tier neighborhoods often climb faster than the incomes needed to support them. Property taxes, maintenance, and renovation costs add to already steep mortgage payments, especially when homes exceed 3,000 square feet or involve historic upkeep.

While home equity may rise, monthly liquidity often tightens. Some households lean on credit for non-housing expenses just to stay flexible. It’s not insolvency—it’s imbalance. Over time, covering expenses through card use becomes routine, making debt less a problem of poverty than of allocation.

9. Dependence on credit rewards programs can encourage excessive use.

Credit rewards can feel like a smart use of spending, with points, miles, or cash back stacking with each swipe. However, optimizing rewards often leads to higher spending overall—as the reward becomes part of the decision process.

In high-income households, this can mean thousands spent for the incremental gain of business-class points or hotel upgrades. When cardholders carry a balance, interest cancels out the perks. The behavior shifts from active choice to passive accrual, embedding debt into the routine of everyday purchases.

10. Supporting adult children financially adds hidden monthly strain.

Parents with adult children may provide rent support, cover education loans, or fund medical costs quietly. Often, those expenses don’t reduce outward lifestyle—meaning the strain lands behind the scenes, on credit lines and emergency savings.

Even when assistance feels optional, the scale can surprise. A $1,200 monthly payment for a child’s apartment, absorbed over three years, becomes more than $40,000. If it’s funded through card advances or delayed reimbursements, balances inch upward. The intent is generosity; the outcome, sometimes, is debt buildup.

11. Social pressure to maintain status drives up spending habits.

Affluent communities often operate under invisible social rules. From car leases to private school fees, the pressure to signal success can infiltrate spending patterns, nudging households to maintain appearances even when budgets feel stretched.

The impact can be subtle. A family might fund a spring gala table or designer wardrobe not out of preference but expectation. When these become recurring costs, credit use rises—not from recklessness, but from quiet conformity. The bill arrives months later, often when attention has shifted.

12. Declines in investment income reduce available funds for payments.

Investment portfolios may generate monthly income, but returns can fluctuate. When the market pulls back, interest-bearing accounts, dividends, or rental profits may fall—reducing the cash on hand to service debts built on better months.

Households that rely on asset income often plan around average gains, not year-to-year dips. A mild downturn might not change core expenses, yet it leaves less buffer for high credit usage. Over time, balances drift upward, not because wealth shrank, but because liquidity lagged behind expectations.