Smart money choices now can help seniors keep control and confidence through shifting economies.

For seniors navigating retirement on a fixed income, economic uncertainty can unsettle even the most carefully laid plans. Inflation, healthcare costs, and market volatility all present real risks to long-term financial stability. By taking proactive steps—from diversifying income to reviewing investment risks—older adults can protect their resources and maintain flexibility. Guidance from experienced financial advisors and data from organizations like the Federal Reserve and OECD can support informed, sustainable choices.

1. Downsize to reduce living expenses and simplify monthly household costs.

Housing often eats up a large share of fixed retirement income, especially when property taxes and utilities stretch thin budgets. Downsizing to a smaller home or apartment can trim those costs substantially, while also lightening the burden of maintenance and upkeep.

Moving from a four-bedroom house to a compact condo can reduce monthly expenses like heating and lawn service, while freeing up equity for medical bills or travel. A tighter space also offers built-in limits on overaccumulating, turning upkeep into something closer to weekend dusting than full-day scrubbing.

2. Diversify income streams with part-time work or rental opportunities.

Relying solely on Social Security leaves many seniors vulnerable when prices rise or unexpected costs appear. Supplementing retirement income with part-time earnings or rental revenue creates breathing room and adds a layer of protection when markets fluctuate or bills spike.

Some retirees find steady income by leasing a basement apartment or monetizing a vacation property during off-seasons. Flexible contract work at a museum or library may also lend routine and purpose—plus modest income—without the pressure of full-time hours.

3. Build a larger emergency fund to cover unexpected life changes.

Unexpected expenses—new prescriptions, household repairs, or family emergencies—can quickly unravel a budget stretched across a fixed income. A well-cushioned emergency fund acts as a financial shock absorber when surprises hit, offering flexibility without dipping into retirement savings prematurely.

Setting aside six to twelve months of essential living costs in a liquid account allows for quick access without penalties. Think of it like keeping an umbrella near the front door—rarely used, but reassuring when a storm rolls in unannounced.

4. Delay major purchases that could strain long-term cash flow.

Big-ticket purchases like new cars, home remodels, or lavish trips can drain retirement accounts faster than expected. Deferring those expenses—especially during unstable markets—helps preserve savings and offers time to reassess whether the purchase still aligns with long-term goals.

If investments dip temporarily, tapping into savings for a luxury upgrade may lock in losses. Waiting even six months can mean the difference between a carefree upgrade and a decision that introduces years of unwanted financial strain.

5. Pay down high-interest debt to lower financial pressure over time.

Debt with high interest—especially on credit cards or unsecured loans—quietly chips away at retirement income each month. Paying it down aggressively reduces long-term burden and helps stretch existing resources further, especially when income is limited by fixed benefits.

For example, a monthly $300 credit card payment may exceed the cost of groceries or utilities and provide no lasting value. Reducing or eliminating that debt returns control over cash flow and cuts stress linked to rising minimum payments.

6. Review monthly subscriptions and cut unnecessary recurring charges.

Recurring bills often blend into the background—TV packages, news apps, boxed deliveries—and quietly siphon cash from a retirement budget. Reviewing each subscription line by line makes it easier to spot services that no longer add value or go unused altogether.

One couple canceled three media services and a monthly mailing service, freeing up over $80 each month. Over a year, that’s enough to cover a heating bill in winter or help cover minor medical copays without rearranging the broader budget.

7. Consolidate financial accounts for easier tracking and better oversight.

Scattered accounts—IRAs, pensions, savings—make retirement finances harder to track and maintain. Consolidating them into fewer accounts simplifies oversight, reduces paperwork, and may also highlight patterns or gaps that affect long-term stability or required distributions.

For example, bringing multiple CDs under one roof can uncover opportunities to ladder maturities or align interest rates. Streamlining also lowers the risk of overlooking fees, missing statements, or forgetting about low-balance accounts tucked away years ago.

8. Automate bill payments to avoid late fees and missed deadlines.

Missing a utility payment or insurance premium by just a few days can trigger fees or bring coverage lapses. Automating payments reduces the manual load and helps protect seniors from oversights that may result from health issues, travel, or memory slips.

A retiree with mild hearing loss might forget a phone-based reminder or misplace a mailed bill. Linking accounts to a reliable checking account ensures steady payments and fewer late charges without requiring constant calendar checks or spreadsheet tracking.

9. Rebalance retirement portfolios to align with current risk tolerance.

Investment portfolios built years ago may no longer match current needs or risk expectations. Rebalancing shifts funds away from volatile assets and toward more stable ones, helping to protect savings from swings that feel more stressful during retirement.

What once worked—like high-growth stocks—may now introduce anxiety rather than returns. A seventy-year-old with fewer income years ahead might favor reliable dividends over speculative gains, especially when withdrawals cover essentials like medication or dental work.

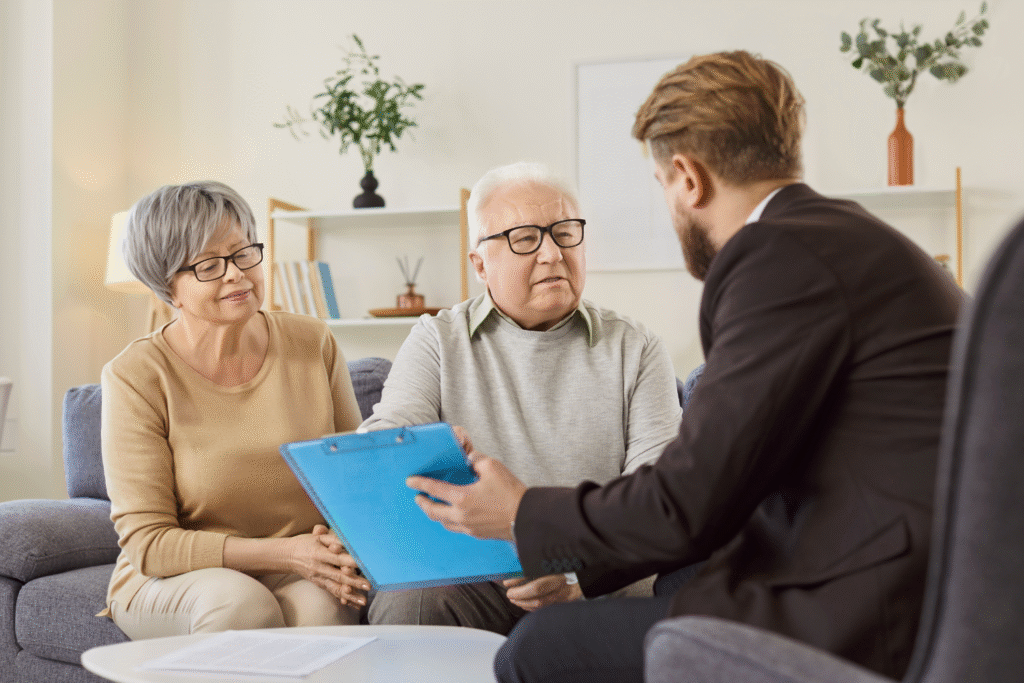

10. Meet with a trusted advisor to review long-term financial priorities.

Long-range planning doesn’t end with retirement. Periodic meetings with a qualified advisor help keep financial goals in sight, correct course as life changes, and ensure that documents like wills or power of attorney reflect current wishes and legal requirements.

One client updated beneficiaries after a family rift and revised medical decision documents. Those updates prevented confusion during a health event and eased the burden on loved ones tasked with handling affairs during a difficult moment.