The hidden costs of daily living that drain retirement savings.

Many retirees assume that once they stop working, their expenses will decrease. However, even without a mortgage or work-related costs, some everyday expenses chip away at their budget faster than they expect. What seems like a small, routine cost can add up significantly over time, leaving retirees wondering where their money went.

Here are 13 regular expenses that can quietly wreck a retirement budget.

1. Eating out too often adds up quickly.

Dining out might seem like an occasional treat, but even a few meals per week can drain a retiree’s budget. A single $15 meal may not feel excessive, but multiplied over several meals a month, it becomes a hefty expense. Seniors living on a fixed income may not realize how much these small indulgences add up, according to Yahoo Finance.

Cooking at home is a much cheaper alternative, but it requires planning and effort. Many retirees opt for convenience over cost, leading to an ever-growing food budget that eats away at their retirement funds faster than they expected.

2. Prescription medications come with hidden costs.

Even with Medicare, prescription medications can be surprisingly expensive. Between co-pays, deductibles, and non-covered drugs, retirees often find themselves spending far more on medications than they initially budgeted. These recurring expenses can take a major toll on long-term savings, according to AARP.

Additionally, medication prices fluctuate, and seniors may not always be aware of cheaper alternatives. Without proactive cost-saving strategies like comparing pharmacy prices or requesting generic options, retirees can end up spending hundreds more than necessary each month.

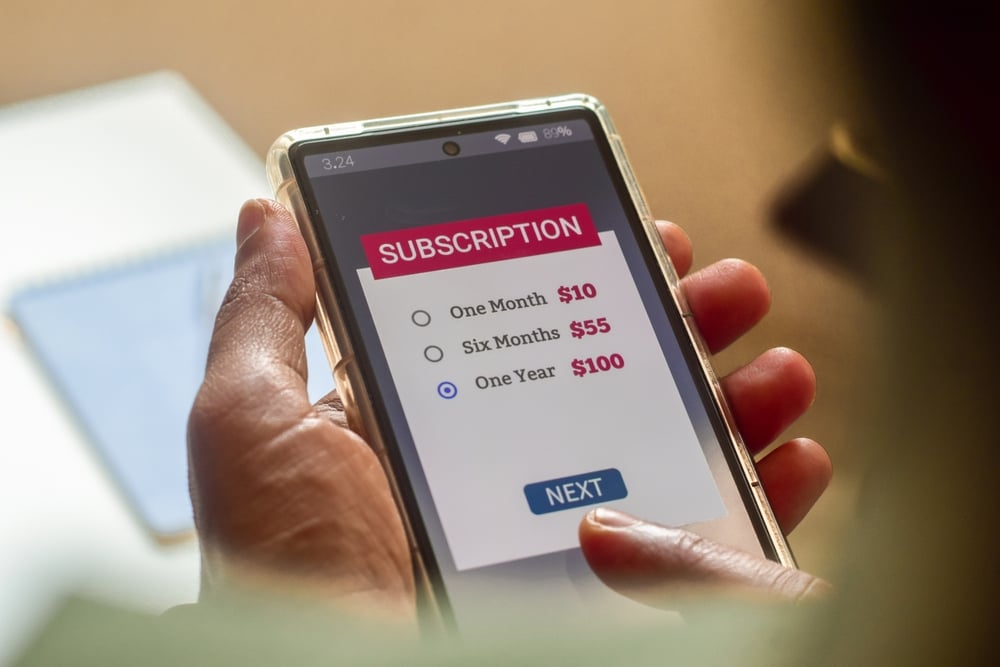

3. Subscription services quietly drain bank accounts.

Streaming services, magazines, meal kits, and other subscriptions often start as small monthly expenses, but they quickly add up. Many retirees forget to cancel services they no longer use, unknowingly paying for things that don’t add value to their lives.

Because these charges are automated, they go unnoticed until the costs pile up. A few $10-$20 subscriptions may not seem like much at first, but over the course of a year, they can easily become an unnecessary financial burden.

4. Home maintenance costs are never-ending.

Owning a home comes with a long list of recurring expenses, from plumbing repairs to appliance replacements. Even if the mortgage is paid off, home upkeep can be a significant financial strain for retirees.

Unexpected expenses like a leaky roof or a failing HVAC system can cost thousands. Seniors who don’t plan for these irregular but necessary repairs can find themselves dipping into their savings more often than they’d like.

5. Groceries are more expensive than they used to be.

Food prices continue to rise, and retirees are feeling the impact. While cooking at home is cheaper than eating out, grocery bills can still take a big bite out of a fixed income, especially for those who prioritize fresh, healthy foods.

Coupons, discount grocery stores, and meal planning can help reduce costs, but many retirees still find themselves spending far more on food than they expected when they first entered retirement.

6. Utility bills can spike unexpectedly.

Electricity, water, and gas bills fluctuate throughout the year, sometimes hitting retirees with uncomfortably high costs. Summer cooling and winter heating costs can be particularly brutal, leaving many seniors scrambling to adjust their budgets.

Energy-efficient appliances, smart thermostats, and simple habits like turning off unused lights can help, but utilities remain a significant and often unpredictable expense.

7. Travel costs can spiral out of control.

Many retirees dream of traveling during their golden years, but even budget-conscious trips can add up quickly. Flights, hotels, dining, and entertainment often cost more than anticipated, making frequent travel financially unsustainable.

Seniors who want to see the world without going broke often opt for off-season travel, house swaps, or RV adventures to cut costs while still enjoying new experiences.

8. Impulse purchases drain savings over time.

Retirees finally have the time to shop, and sometimes that leads to unnecessary spending. Whether it’s an expensive hobby, home décor, or “treating the grandkids,” these small purchases add up.

Frugal retirees set clear spending limits and avoid impulsive buys, ensuring they stay within their budget without sacrificing financial security.

9. Charitable donations can add up unexpectedly.

Seniors tend to be generous, but frequent donations—even small ones—can put a dent in their budget. Many retirees receive constant requests for contributions from charities, and saying yes too often can become costly.

Setting an annual donation budget ensures that generosity doesn’t compromise financial stability. Giving is important, but it should always align with overall financial goals.

10. Cell phone and internet bills are higher than necessary.

Many retirees overpay for mobile and internet plans that far exceed their needs. Some continue paying for premium services, unlimited data, or multiple streaming platforms they barely use.

By reviewing their plans and switching to lower-cost alternatives, retirees can save hundreds per year without sacrificing connectivity.

11. Unexpected family financial requests can drain savings.

Retirees often find themselves financially supporting adult children or grandchildren. Whether it’s covering rent, student loans, or unexpected emergencies, these financial obligations can quickly become overwhelming.

Setting firm boundaries and offering financial guidance instead of direct cash assistance can help seniors protect their own financial future while still supporting loved ones.

12. Insurance premiums continue to rise.

Health, home, and auto insurance costs tend to increase with age. Many retirees don’t regularly compare rates or adjust their policies, leading to unnecessary overspending.

Shopping around for competitive rates and adjusting coverage as needed can significantly reduce these recurring expenses.

13. Personal care and salon visits add up.

Haircuts, nail appointments, and skincare treatments might not seem expensive at first, but over time, they can become a significant cost. Many retirees continue their pre-retirement self-care habits without realizing how much they’re spending annually.

Switching to at-home alternatives or stretching out the time between appointments can help retirees keep looking their best without overspending.