Why some financial missteps still led Baby Boomers to outpace Millennials in long-term wealth

Baby Boomers didn’t always make perfect financial decisions, but many still built lasting wealth. Their path was shaped by lower home prices, affordable college costs, and widespread job stability factors that are far less accessible to Millennials today. Even outdated habits like paying off a mortgage early or skipping credit cards sometimes paid off under different economic conditions. Understanding how context buffered their mistakes can help younger generations adapt smarter, more flexible strategies.

1. Buying more house than they realistically needed or could maintain.

Larger homes once signaled financial success, even if utility bills stretched budgets or upkeep drained time. Many Boomers bought houses with more square footage than needed, choosing space over efficiency. A formal dining room sat unused while property taxes crept up year after year.

Despite the mismatch, rising property values often bailed them out. A modest house in 1970 could triple in value by retirement, covering lean years or funding downsizing with a cushion. Millennials, facing tighter markets and zoning constraints, rarely see such leveraged returns on overbuying.

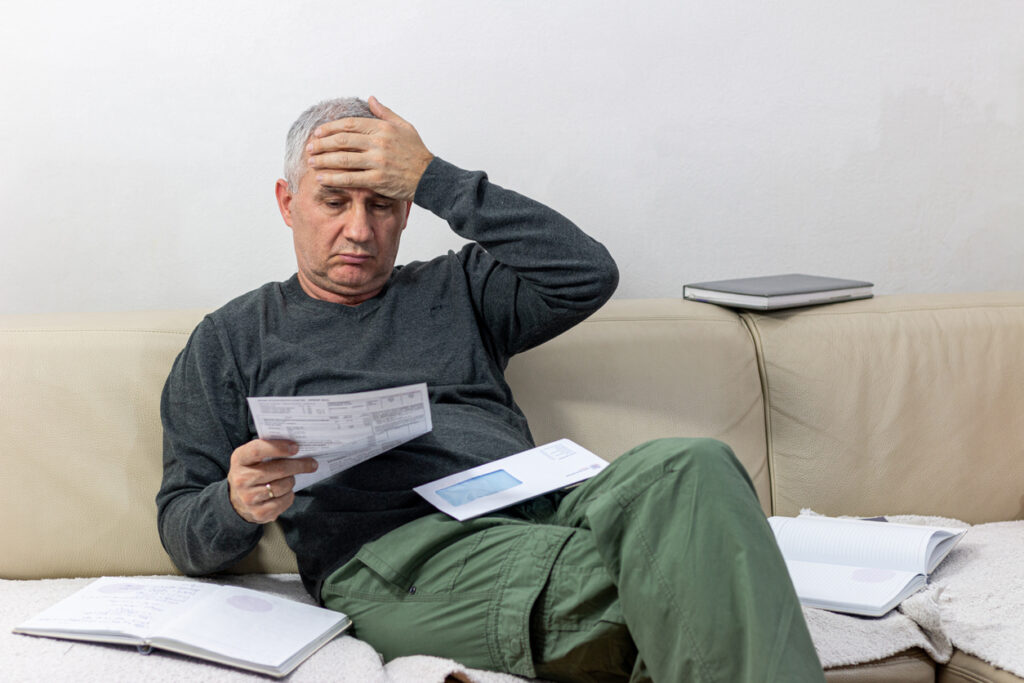

2. Paying off mortgages early instead of investing in higher-growth assets.

For mid-century households, paying off the mortgage early felt prudent—owning a home outright conferred stability. Boomers often chose that path even when mortgage rates fell or better investment yields surfaced. Peace of mind sometimes outweighed math-based opportunity.

As markets expanded, early payoff meant missing higher returns from stocks or long-term funds. Still, decades later, many Boomers owned valuable homes free and clear, a level of equity that shielded them from inflation or job loss. Millennials often face student debt instead, with no asset gain in return.

3. Prioritizing job stability over pursuing career growth or passions.

In an era of pension loyalty, sticking with steady jobs was seen as smart. Boomer workers often accepted slow promotions or uninspiring roles in exchange for reliable checks and retirement packages. A steel factory’s hum or government cubicle’s buzz was familiar, if unglamorous.

That consistency, paired with rising wages and employer-provided benefits, built savings over time. For Millennials, gig work and at-will contracts replaced such paths, making long-term planning harder. Career mobility now often replaces the financial security those single-track roles once offered.

4. Sticking with a single employer too long and missing better offers.

Many Boomers grew up with postwar norms that favored lifetime employment. Loyalty often meant waiting decades for raises while better offers went unanswered. Staying put seemed safer than jumping at what might not last.

In hindsight, some missed lucrative pivots, but tenure often paid off. Defined pensions and vested stock options ultimately rewarded long stays. For Millennials, job-hopping has become necessary for wage growth, yet it rarely carries the same structural financial rewards once offered to long-tenured Boomer employees.

5. Avoiding credit cards entirely rather than learning to manage them wisely.

Some avoided credit cards entirely, fearful of debt spirals or hidden fees. Raised on cash and checks, Boomers often chose to operate without building credit, mistrusting plastic even for small purchases.

Though this sidelined them from rewards programs or score boosts, their minimalist approach also dodged major financial traps. Fast forward, younger adults face complex systems where credit history shapes housing access and loan terms. Austerity once helped Boomers avoid traps, even as it left some credit-invisible.

6. Refusing to discuss finances openly, even with close family members.

Cultural norms once discouraged open money talk, even within families. Boomer parents often kept details of debts, inheritances, or salary changes private, creating invisible lines around financial stress or windfalls.

That silence sometimes prevented early financial literacy or estate planning collaboration. Still, steady pensions or paid-off homes cushioned retirement outcomes. Millennials, raised in an age of shared spreadsheets and financial podcasts, navigate a climate where silence can obscure risks—though privacy once protected Boomers from social comparison’s churn.

7. Saving aggressively but keeping too much money in low-interest accounts.

Boomers sometimes stockpiled cash in savings accounts long after interest rates dropped. Trust in banks over markets led to large balances in passbook accounts earning barely more than inflation. The habit came from an era when 5-percent returns were normal.

Inflation erosion bit quietly, but consistent deposits still built emergency reserves. That cushion allowed many to weather job losses or health setbacks. Millennials, navigating student debt and rising rents, often save less—though they’re likelier to seek growth in equities or digital alternatives.

8. Following outdated budgeting advice that ignored rising living costs.

Budgeting books from the 1980s touted fixed percentages for food, housing, and leisure. Boomers embraced these tidy formulas, often skipping ongoing recalibration as costs for healthcare, education, and rent outpaced old models. Advice meant for one economy mismatched rapid shifts in another.

Still, that outdated structure sometimes fostered discipline. Envelope systems and paycheck splitting became habits, regardless of rising utility bills or shifting job markets. Millennials often face dynamic costs that resist static plans, making rigid templates less effective now than they once seemed.

9. Investing heavily in physical assets without properly diversifying portfolios.

A strong belief in property, antiques, or gold led some Boomers to overconcentrate. Trusting tangible goods over abstract indexes, they sometimes skipped stocks or bonds entirely. A coin collection glinting in a cedar chest might have seemed safer than mutual funds.

Appreciation in home values or rare art occasionally rewarded this bias. But others missed the broader market booms that diversified investors enjoyed. Millennials, less able to afford entry into physical assets, often rely more on ETFs or crypto, with different risk and volatility profiles.

10. Delaying retirement planning despite steady long-term income opportunities.

Even with stable careers and home equity, many Boomers waited too long to organize retirement. A belief that pensions or Social Security would fill gaps delayed deeper planning. Retirement felt far off until colleagues suddenly turned 65.

Late starts sometimes meant sacrifices, but long job tenure and union-backed benefits buffered the impact. By contrast, Millennials often began hearing about retirement planning early—yet faced fewer employer pensions and more financial insecurity, making early action harder to afford despite greater awareness.